Trump vs. the Fed: Should interest rates drop?

Trump vs. the Fed: Should interest rates drop?

One of 2025’s biggest economic dramas has been the battle between President Donald Trump and Federal Reserve Chairman Jerome Powell over the central bank’s interest-rate policy.

Trump has been less than subtle in urging the Fed to cut the rates it controls. Powell, in what has been a rare pushback against Trump among federal policymakers, insists it’s still too early to cut rates.

You see, one of the Fed’s responsibilities is to act as a cost-of-living watchdog for the nation. And while Powell admits that inflation is muted, Trump’s tariff policies are muddying the picture of what consumers will soon pay for imported goods.

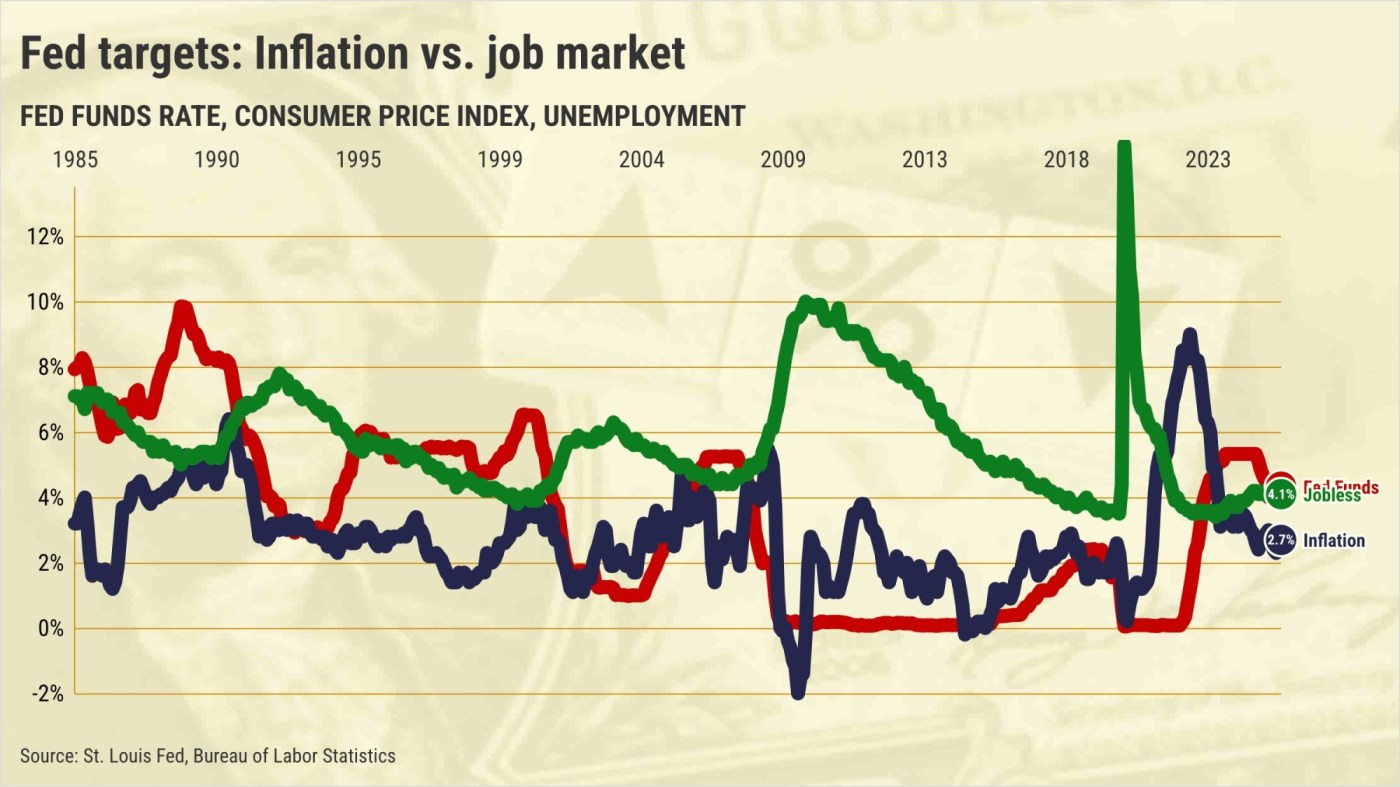

The politically independent Fed sets an economic pace with its so-called “Fed Funds” rate. Tweaking what banks charge each other for overnight loans usually dictates the cost of short-term money.

Those costs can alter the economy’s path. High rates tend to cool business activity. Low rates stimulate it.

So the debate is really how much help – if any – does the economy require?

This Tuesday and Wednesday, central bankers will gather to update the Fed’s interest-rate intentions. The arguments should be heated, but the bet is that the central bank will make no change for now.

My trusty spreadsheet examined several key economic markers, comparing their latest readings with their 40-year median to find hints at what’s behind this dispute.

There’s inflation. It’s down, but is it cured – especially with Trump’s tariffs on imported goods yet to fully hit the economy?

The Fed’s “dual mandate” means it also oversees the nation’s job market. U.S. unemployment remains low with joblessness at 4.1% in June, below the 5.4% historical norm.

This worker shortage poses a challenge. Bosses must battle for talent, and what they pay is a weapon in that struggle.

Look at weekly wages, as measured by average earnings of production and nonsupervisory employees in the private sector. This compensation marker grew at a 3.3% annual pace in June, compared with 3% raises over the past 40 years.

That pay premium may be trouble for corporate bottom lines and inflation.

Cheaper money can put consumers and corporations in a buying mood, and it can lower the nation’s deficit-riddled budget’s borrowing costs.

Yet do not forget what happened during the pandemic when ultra-low rates and stimulus checks combined with supply-chain shocks to push inflation to a four-decade high.

Additionally, recent tax-cut legislation is expected to provide incentives for businesses to expand.

The president and other Powell critics note the rates the Fed controls haven’t been this high since 2007.

In June, the Fed Funds rate ran at 4.3% – above the 3.2% median since 1985. Therefore, the central bank has applied a modest brake to the economy.

Curiously, they’re sort of complimenting Powell. The high-rate policy, introduced in 2022, has mitigated problematic inflation.

In June, the Consumer Price Index showed inflation at a 2.7% annual rate, matching its 40-year average. Powell critics argue the cost of living is in check.

Also, eyeball the broader economy. U.S. business output was growing at a 2.6% annual pace in June, according to a Philadelphia Fed index. That’s below the 3.1% historical pace. Lethargy justifies lower interest rates.

And lofty borrowing costs have muffled businesses that rely on financing deals. Think real estate.

The 30-year fixed mortgage rate ran 6.5% in June, according to Freddie Mac. That’s more than double what was charged four years ago, during the pandemic. But it’s also below the 6.8% 40-year median.

So, U.S. home prices cool mildly. House values were growing at a 3.1% annual rate in April, the latest result from the Case-Shiller index. That compares to historic gains of 5.4%.

The Fed is only one part of the economic equation.

No guarantees exist that other forces – notably the bond market – will go along with nudges to create cheaper loans.

Bonds are essentially loans that trade on Wall Street. Investors want to get repaid with an interest rate that compensates them for the risk and inflation.

So, bond traders think differently from the average person about longer-term interest rates – including mortgages.

Contemplate one key long-term rate: the yield on 10-year Treasury bonds. It ran 4.4% in June. That’s essentially equal to its historical norm.

Oddly, that’s also roughly the short-term Fed Funds rate. You see, over the past 40 years, 10-year bonds have yielded 1.4 percentage points more than the Fed Funds rate.

This rarity suggests, at the very least, economic uncertainty.

And how might long-term bond traders get back to the traditional spread above short-term rates?

If traders share similar anxieties over inflation as the Fed chairman, they may not lower their demands for yield after cuts in short-term rates.

Right or wrong, the stock market is often seen as a sounding board for economic policy.

And stock traders appear to have become accustomed to the great rate debate.

After some early spring gyrations, the stock market’s benchmark S&P 500 index was growing at a 12% annual rate in June.

However, note that such bullishness is actually below average. The index’s median result has been 15% annual gains since 1985.

Jonathan Lansner is the business columnist for the Southern California News Group. He can be reached at jlansner@scng.com

With Beyoncé's Grammy Wins, Black Women in Country Are Finally Getting Their Due

February 17, 2025

Comments 0